Sub-$2 gas prices at the US benchmark Henry Hub are putting operators in the Haynesville Shale under the gun recently, raising questions about the potential for a slowdown in drilling and production there.

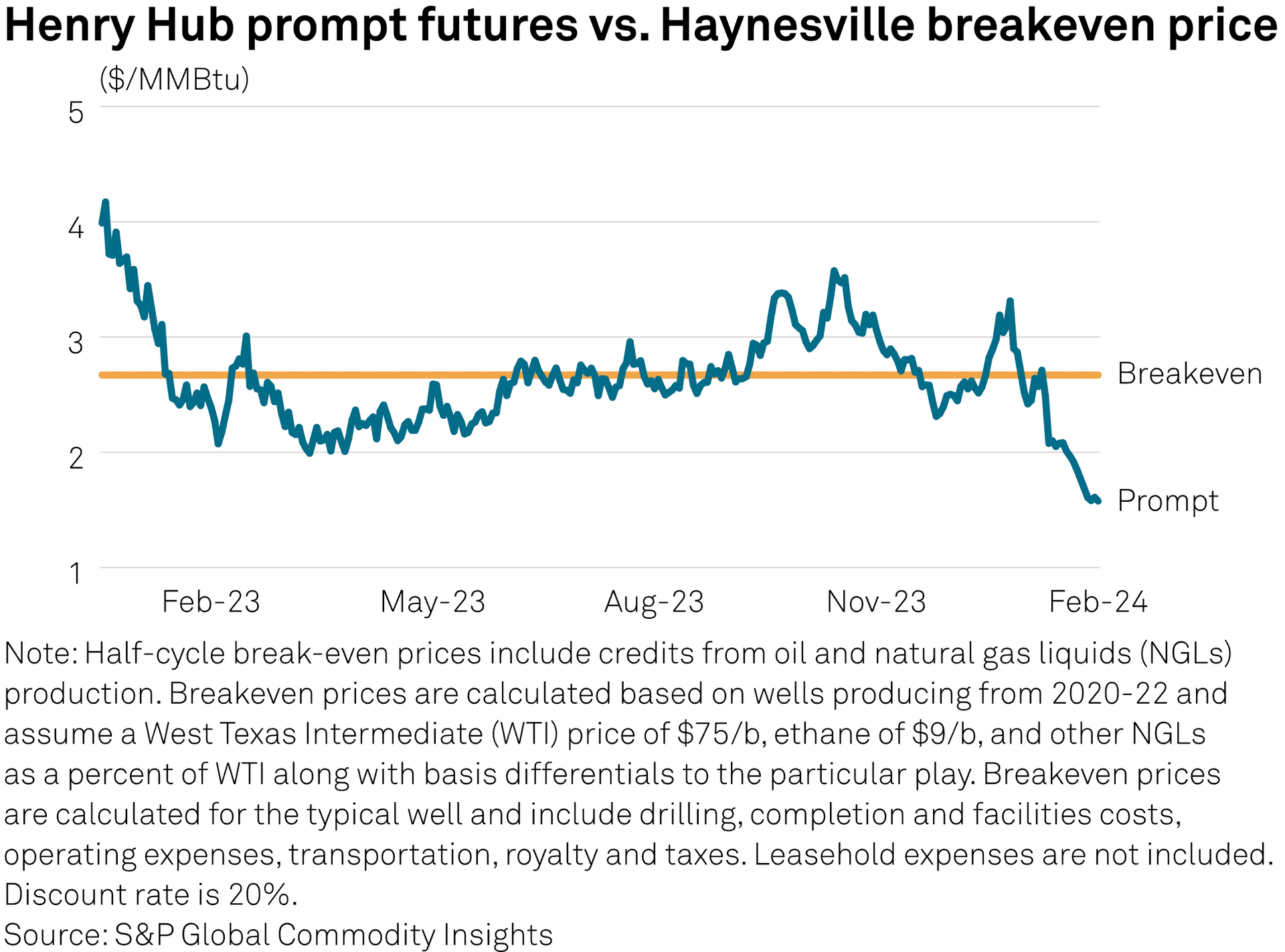

In 2024, NYMEX prompt-month gas futures have averaged just $2.35/MMBtu to trend at their lowest year-to-date price since 2020. Over the past four weeks, mild US temperatures, flagging gas demand and bearish weather forecasts have sent futures prices even lower. On the NYMEX, the prompt-month gas contract is down more than 45% from the upper-$2 area in late January, testing a new low recently at just over $1.50/MMBtu, data from S&P Global Commodity Insights showed.

In the Haynesville Shale, many, if not most, producers are already feeling the price pain this year.

Even for highly efficient operators with the highest-quality acreage, the Henry Hub breakeven price for Haynesville gas is currently estimated at $2.67/MMBtu. For producers looking to return 30% free cash flow -- a reasonable metric for Wall Street investors these days -- that wellhead clearing price rises to $3.21/MMBtu for class-1 and $3.57/MMBtu for class-2 acreage, S&P Global Commodity Insights estimate show.

Supply outlook

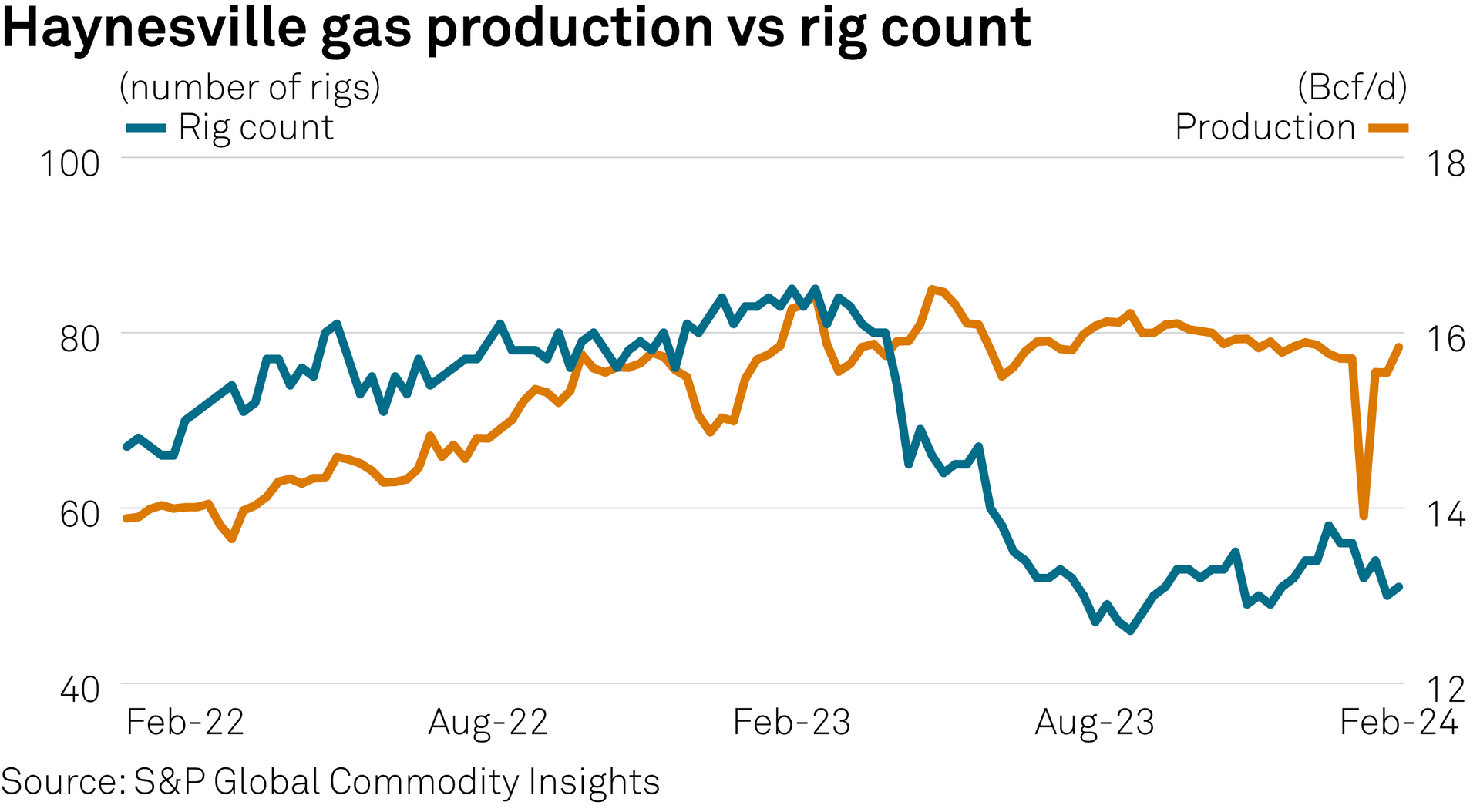

According to a first-quarter supply outlook published in January by S&P Global, gas production in the Haynesville is expected to remain roughly flat this year at just over 15 Bcf/d. Producers there are expected to run an average of 47 rigs, which would amount to a more than 10% drop from the current year-to-date average of 53 rigs. In the week to Feb. 14, the Haynesville rig count dropped by three to 49, hitting its lowest since mid-November, data from S&P Global showed.

With Henry Hub futures pricing below $2 through March, April and May, however, there could be a downside risk, even to the roughly flat production outlook for 2024.

"I think below $2 price outlook will change the way operators manage new drilling activities and backlog DUC well completions for the upcoming LNG growth," said Narmadha Navaneethan, senior lead of equity research and fixed income for S&P Global. "With squeeze in cash flows, we will see rigs drop, especially by the privates," she said.

Producer guidance

On recent fourth-quarter earnings calls, a number of public Haynesville operators have said they intend to pare capital spending, drilling and completion activity this year in response to oversupplied market conditions.

Chesapeake Energy plans to drop one rig in March to four total within the Haynesville, and the company has already let one frack crew go in the basin, leaving one operating.

To drive production declines, Chesapeake said it will effectively pause turn-in-lines while still building its inventory of drilled but uncompleted wells throughout the year. Full-year Haynesville production is expected to average just shy of 1.2 Bcf/d, down about 400 MMcf/d from its 2023 in-basin average.

The market is "pretty clearly telling us that it doesn't need our gas today," Chesapeake CEO Nick Dell'Osso told investors and analysts on a Feb. 21 conference call.

Competitor Comstock Resources recently released one of the seven rigs it brought into the new year and will drop another in the first quarter, according to full-year guidance detailed Feb. 15. After exiting Q4 2023 producing 1.5 Bcf/d, Comstock expects output to keep flat through the first half of the year before declining in the second half.

2025 outlook

The decision to dial back activity this year could be expected to impair Haynesville producers in 2025, according to Siebert analyst Gabriele Sorbara.

"It's going to be a headwind for a few companies that are slowing down this year, managing and staying within free cash flow, but that will be obviously positive for the macro next year in prices," Sorbara said.

Outside of the Haynesville, producers including EQT and Range Resources have held off on materially cutting capital and rigs, hoping to position themselves for the upside associated with new LNG capacity that's projected to begin coming online later this year and throughout 2025.

With the addition of Golden Pass LNG and Plaquemines LNG, close to 8 Bcf/d in new feedgas demand is expected to arrive between September 2024 and January 2026, according to S&P Global gas market analysts.

Tom Jorden, CEO of Marcellus producer Coterra Energy, acknowledged that the company's decision to slash 2024 spending in the basin by more than $400 million could set the company back once gas prices rerate but that capital would be put to better use on its operations in the Permian and Anadarko for now.

"Missing a few months of the recovery is much better than fully participating in the downside," Jorden told analysts on a Feb. 23 conference call.

Contact Us:

info@iadd-intl.org

3322 Hideaway Lane

Spring, TX 77388