North America Directional Drilling Market Analysis

The North America Directional drilling market is projected to register a CAGR of over 4.5% during the forecast period (2022-2027).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

- Over the long term, drilling in unconventional reserves, which involves directional or horizontal type drilling to increase contact with the pay zone along with increased production, is expected to drive the growth of the market studied.

- On the other hand, high volatility of crude oil prices and low-price scenarios is expected to restrain the growth of the Directional drilling maWith technological

- Nevertheless, with technological improvements and increasing viability of deepwater and ultra-deepwater projects, several new markets, such as the Gulf of Mexico actively promoting the development of deepwater and ultra-deepwater reserves are likely to provide an excellent opportunity in the forecast period.

- United States dominates the market and is also likely to witness the highest CAGR during the forecast period. In recent years the United States has emerged as a major crude oil and natural gas producer in the world, and the country is expected to maintain this during the forecast period.

North America Directional Drilling Industry Segmentation

Directional drilling is a technique used by oil-extraction companies in order to access oil in underground reserves. Directional drilling is also called directional boring. Most oil wells are positioned above the targeted reservoir, so accessing them involves drilling vertically from the surface through to the well below. The directional drilling market is segmented by service type, location of deployment, and geography. By service type, the market is segmented into rotary steerable systems, and conventional. By location of deployment, the market is segmented into onshore, and offshore. The report also covers the market size and forecasts for the Directional drilling market across major countries. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

North America Directional Drilling Market Trends

This section covers the major market trends shaping the North America Directional Drilling Market according to our research experts:

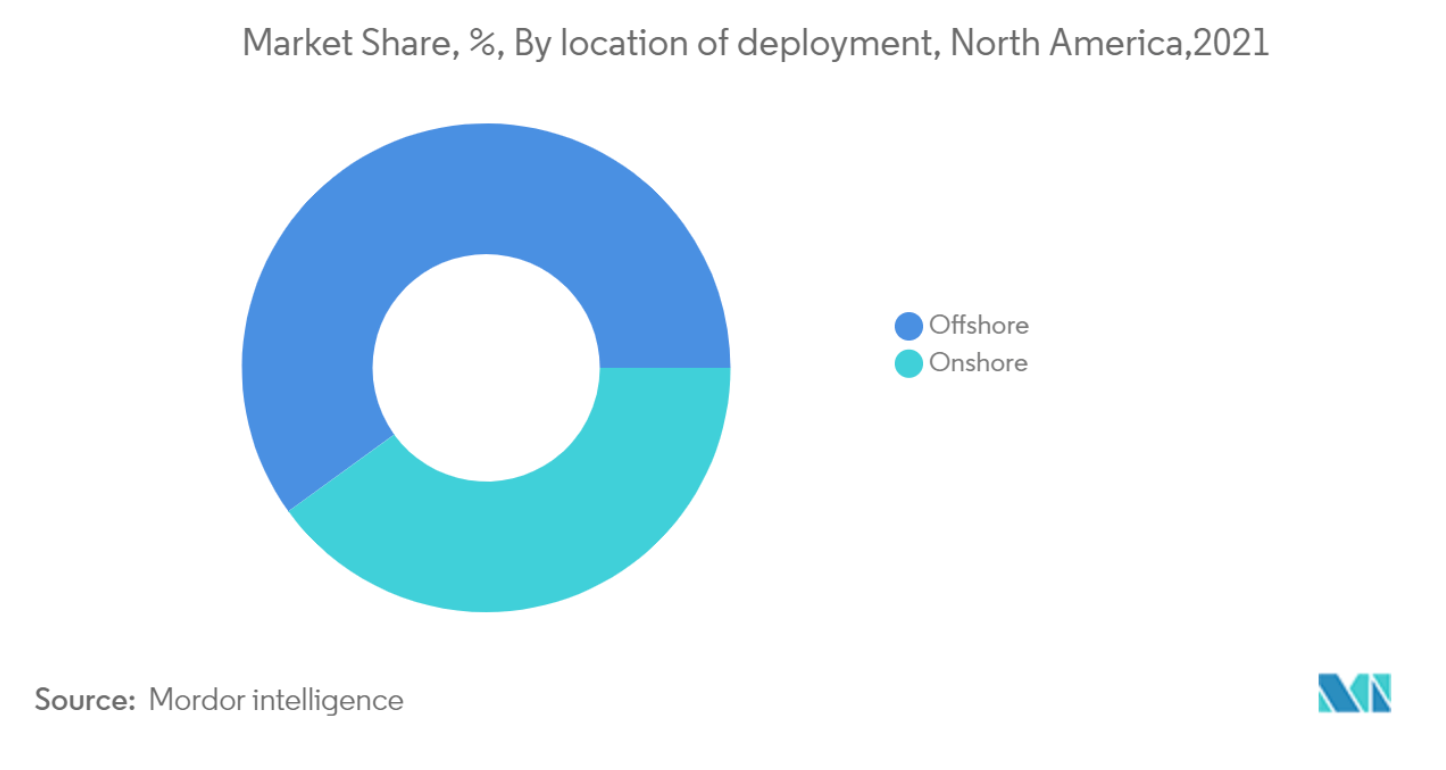

Offshore Segment Expected to Witness Significant Demand

- The offshore oil & gas industry accounts for about 30% of North American crude oil production. The Gulf of Mexico are the major offshore oil and gas producing region. In addition, the availability of abundant resources, coupled with increased potential to recover oil and gas from deepwater and ultra-deepwater areas, is expected to provide an excellent opportunity for the directional drilling market.

- Deepwater oil production is concentrated in four countries – Angola, Brazil, Nigeria, and the United States. During the past years, deepwater investments have retained a significant share, reflecting opportunities in the Gulf of Mexico and offshore Latin America (Brazil and Guyana).

- In Canada's Saskatchewan region, the upstream capital expenditure in 2021 is expected to increase by 5%, to USD 2.8 billion in 2021 from an estimated USD 2.7 billion in 2020. The Saskatchewan Party government's Vision 2030 aims to increase oil production by 25% to 600,000 bpd by 2030, along with fiscal incentives that enhance investment attractiveness for the industry players. Moreover, in Alberta, which produced about 65% of Canada's natural gas and 82% of the country's oil in 2020, the upstream investment is expected to increase by 18% to USD 11.8 billion in 2021 from 2020.

- Mexico's crude oil and natural gas production has been declining since 2005. To address the decline, the former government introduced energy reforms ending the 75-year monopoly of PEMEX, a state-owned oil and gas company, to attract foreign investment in exploration and development projects.

- There has been an increase in offshore exploration and production (E&P) activity recently because of the expanding number of maturing onshore oilfields. Although production from older wells has begun to drop, and there is little room for fresh discoveries in certain regions, the Permian Basin of the United States is the most significant in crude oil production in the nation. To fulfil the rising demand, the oil and gas industry is a result of turning its attention to deeper locations in quest of oil and gas.

- In May 2022, US Environmental Protection Agency will invest USD 53 Million in the Gulf of Mexico through the Bipartisan Infrastructure Law (BIL). This investment will provide over USD 10 million in funding per year through 2026 and will support wetland restoration, stormwater treatment and control, nature-based infrastructure, resilient shorelines, and other initiatives critical to creating a healthy and vibrate Gulf of Mexico.

- Hence, owing to the above points, increasing investment in the offshore segment will drive the market during the forecast period.

The United States is fastest growing region

- North America is one of the largest markets in terms of capital expenditure infused in the oil and gas industry. The United States is the leader, followed by Canada and Mexico. The United States is a major crude oil and natural gas producer in the world, and the country is expected to cover around 60% of the world oil demand in the coming years if shale oil and gas production follows the same trend as was witnessed before 2020

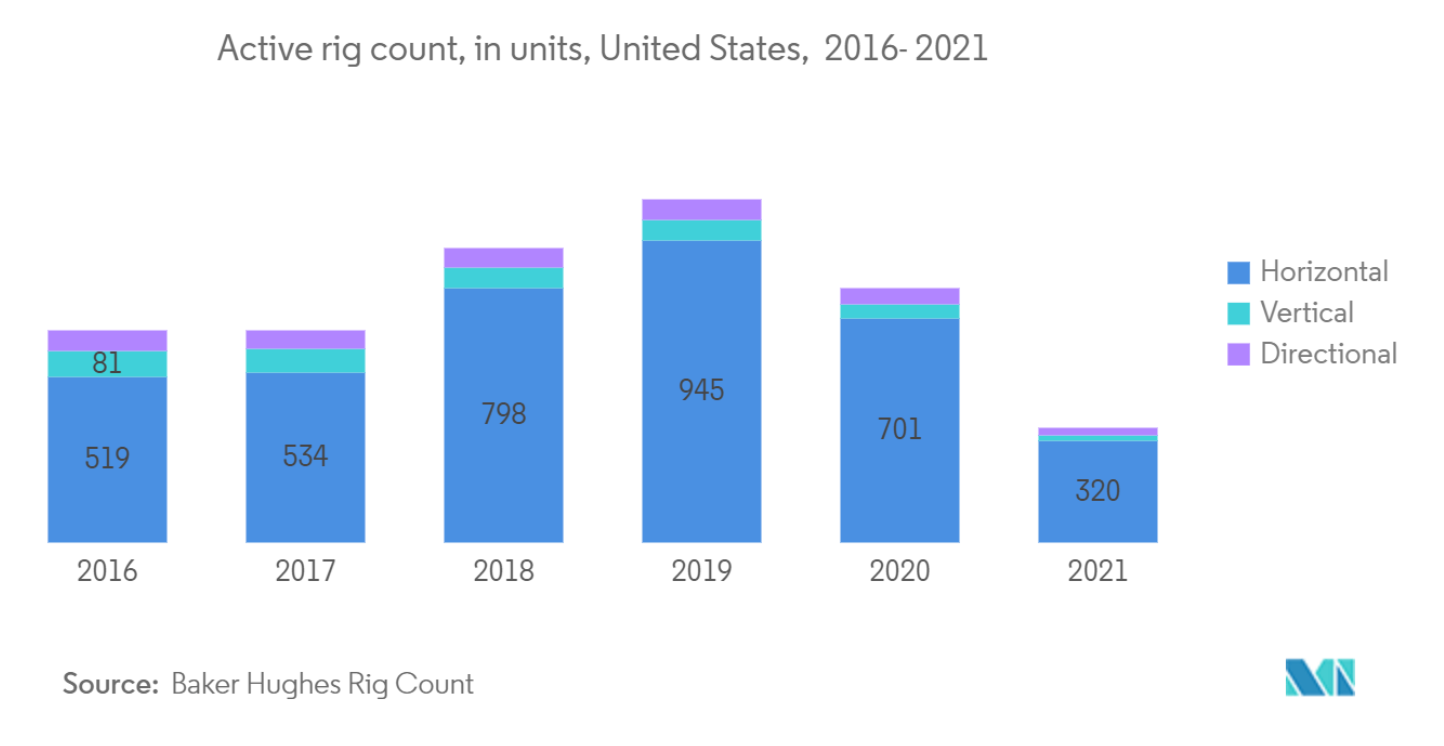

- As of July 15th, 2022, the United States has a total of 756 active rotary rigs, of which 14 are offshore rigs, 4 Inland water rigs, and 738 onshore rigs. A rotary rig is considered occupied when the rig is on the location and is drilling the majority of the week (4 days out of 7 days). This indicates the dominance of fixed assets such as drilling rigs and production platforms in the upstream segment of the country.

- In the offshore upstream segment, floating rigs are often used for exploratory drilling and drilling in waters deeper than 3,000 feet. As of June 2022, the United States stood among the top three countries worldwide in the demand for floating assets (semisubmersibles and drillships).

- According to the United States Geological Survey (USGS), over 46 billion barrels of oil, 280 trillion cubic feet of gas, and 20 billion barrels of natural gas liquids are trapped in the low-permeability shale formations of the United States. These fields must be explored and produced to fulfil the increasing demand for oil and gas.

- From 2008 to 2021, the share of shale gas in total natural gas production in the United States increased from 16% to 70%. During the forecast period, shale gas is expected to continue driving the growth of natural gas production in the country, owing to increasing technological developments in drilling and completion, particularly in the areas of horizontal drilling and hydraulic fracturing.

- Hence, owing to the above points, the United States is expected to see significant growth in the Directional drilling market during the forecast period.

North America Directional Drilling Industry Overview

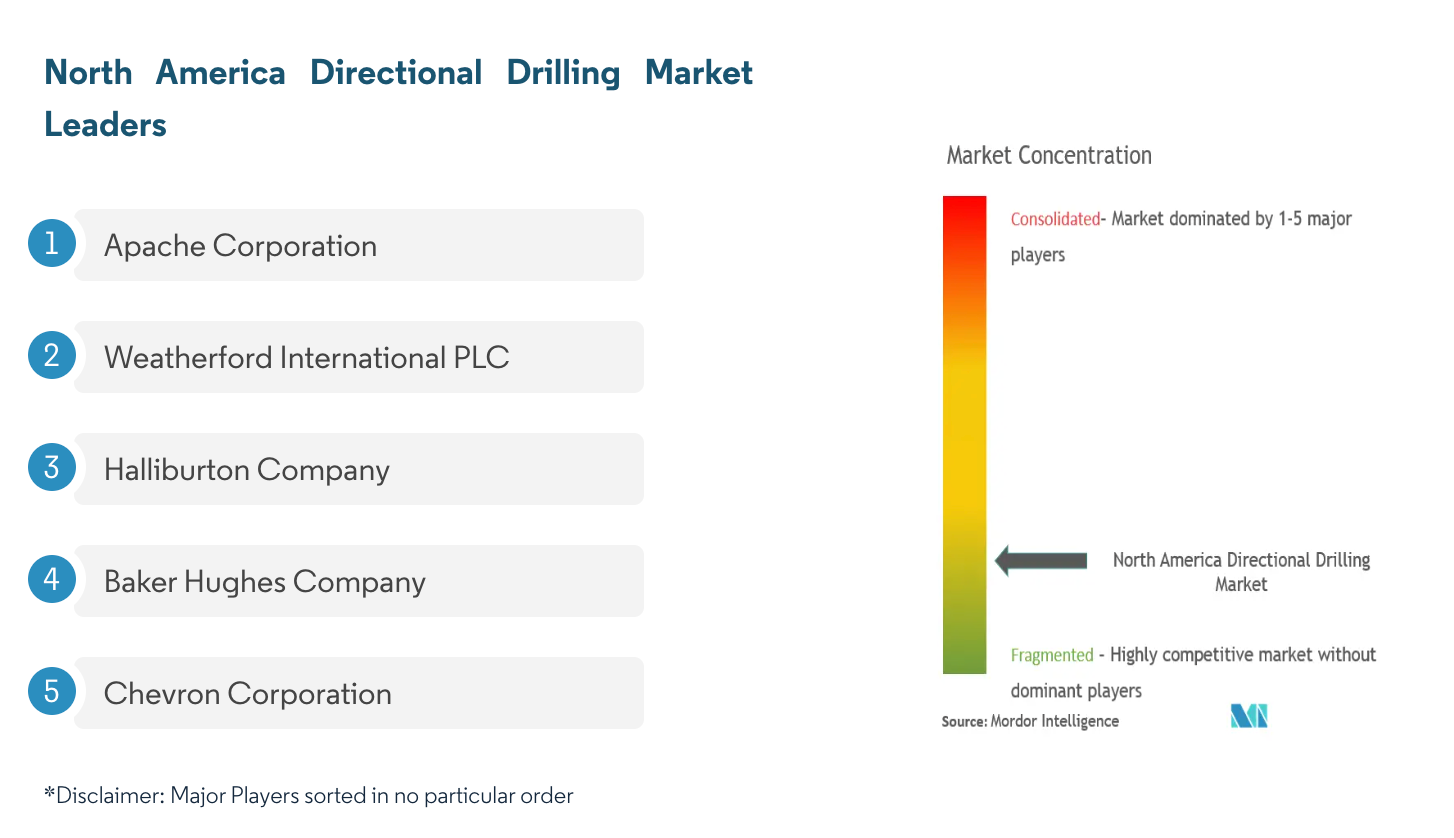

The North America Directional drilling market is moderately fragmented. Some of the key players in this market (in no particular order) include are Apache Corporation, Weatherford International PLC, Halliburton Company, Baker Hughes Company, and Chevron Corporation.

North America Directional Drilling Market Leaders

North America Directional Drilling Market News

- In November 2021, Nabors Industries Ltd came into a contractual agreement with Chesapeake Energy Corporation to choose Nabors as the preferred drilling contractor for the oil and gas projects in the United States. This agreement is likely to enable the company to expand its business portfolio across the country.

- In August 2021, Michels Canada extended the limits of trenchless construction in Canada by using horizontal directional drilling (HDD) to complete a 3540 m crossing in Burlington, Ontario, under the Hidden Lake Golf Club. The installation is part of Imperial’s Waterdown to Finch Project, a proactive replacement of approximately 63 km of the Sarnia Products Pipeline between the Waterdown pump station in rural Hamilton and the storage facility in Toronto’s North York area. The Hidden Lake HDD is the longest successful HDD installation in Canada to date, surpassing the previous record of 2195 m, also set by Michels Canada.

Contact Us:

info@iadd-intl.org

3322 Hideaway Lane

Spring, TX 77388