- Supermajors' refining, retail arms cut need to use derivatives

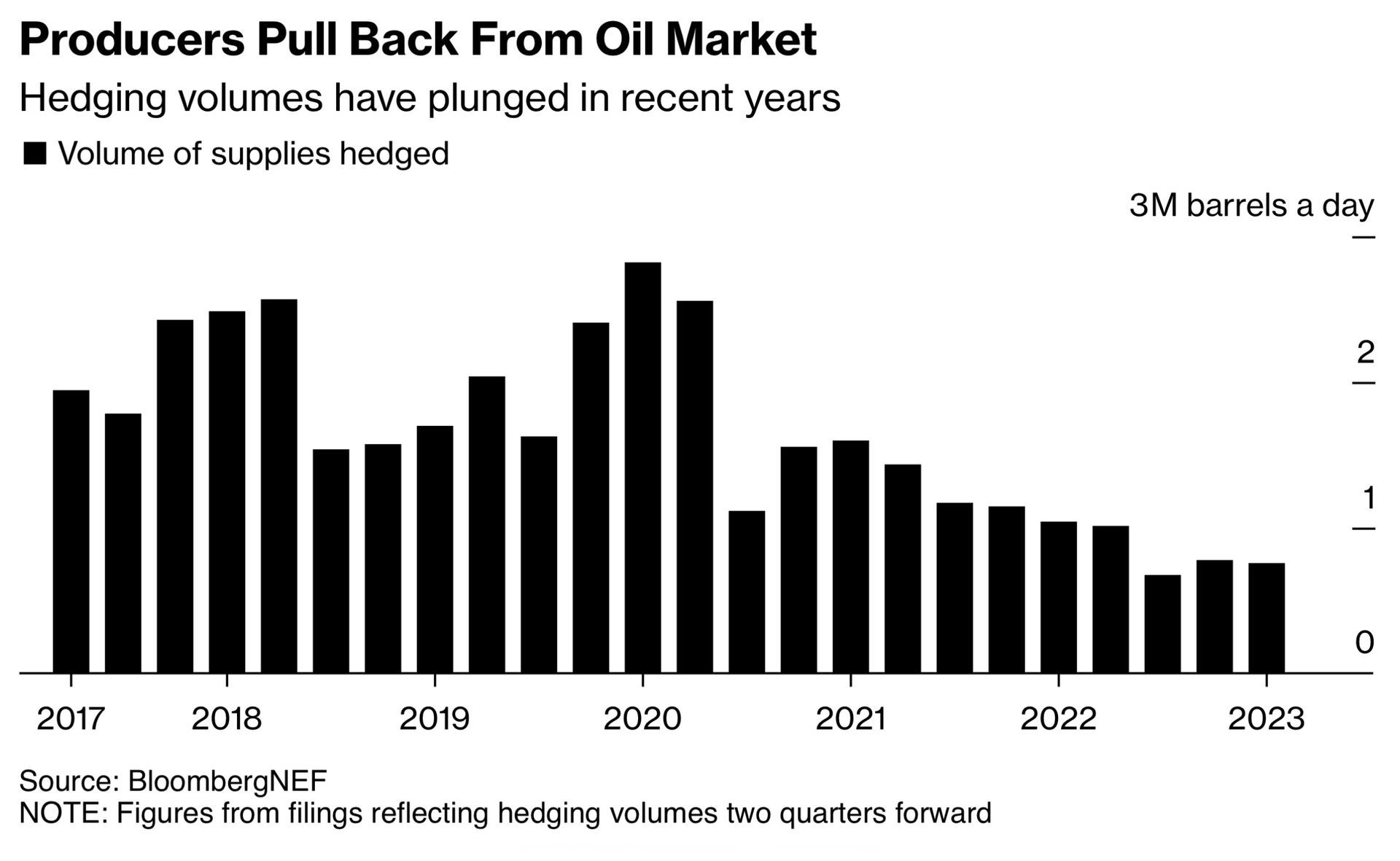

- Producers have reduced market activity in recent years

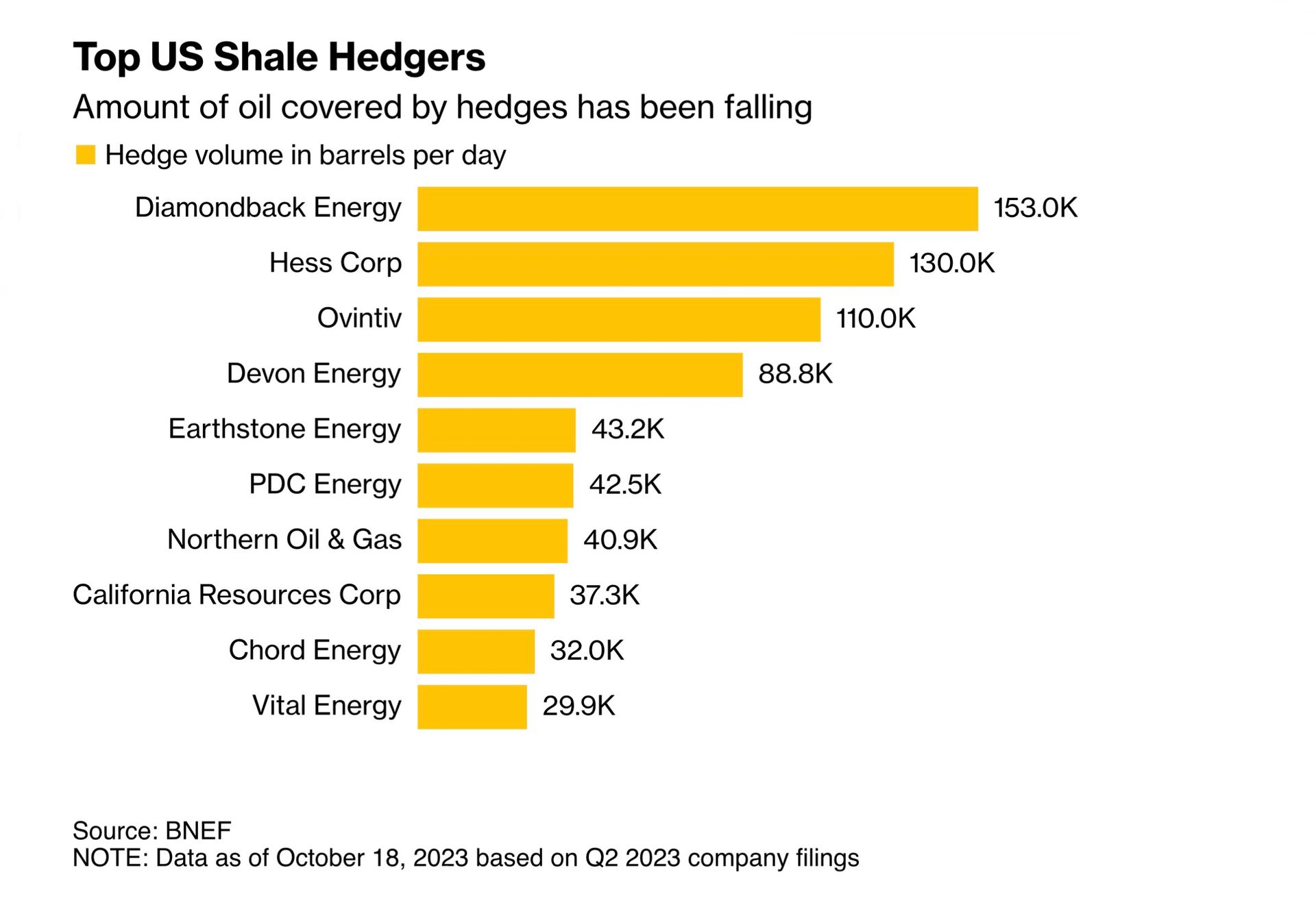

Hess Corp. and Pioneer Natural Resources Co. have in recent years bought large derivatives positions to lock in prices for their future production. Those holdings are set to dry up after the drillers' takeovers by Chevron Corp. and Exxon Mobil Corp. because super majors tend to not hedge, instead using their refining and retail operations as natural buffers against price moves. Two other top hedgers - Devon Energy Corp. and Marathon Oil Corp. - are also said to have held merger talks.

The consolidation threatens to accelerate a decline in listed producers' activity in the oil derivatives market, potentially increasing volatility and exposing drillers to steeper earnings drops in the event of a price crash. US oil producers had about 750,000 barrels a day of supplies locked in using derivatives contracts in the first quarter, down more than two thirds since before the pandemic, according to data from BloombergNEF. Those are near the lowest levels in data dating back to 2017.

Oil producers typically use derivative contracts such as swaps and options to cover production about 24 months or more into the future, guaranteeing their revenues even if prices slump. The practice provides crucial liquidity for the more distant oil futures contracts and spurs active trading in the instruments, where participation is otherwise thin.

Hess had locked in prices for about 130,000 barrels a day of production for the rest of 2023, according to its most recent press release. That is the second largest volume of producer hedges in the US, according to BloombergNEF data. While Pioneer had only 3,000 barrels a day of production hedged as of the end of June this year, it had locked in about 175,000 barrels a day for 2021 by the end of 2020.

An additional 100,000 barrels a day would be lost if Devon and Marathon merged and chose not to hedge, based on the companies' previous activity.

Diamondback Energy was the largest hedger at 153,000 barrels a day, accounting for about one of every five barrels that has been hedged.

As hedgers become more rare, the futures curve can become increasingly flattened during a rally because of the absence of natural sellers in the back end. In an unlikely event where oil prices crash suddenly into the $50s or even lower, the move to leave production uninsured could prove costly and eat into earnings.

"In principle, the reduction in hedging from the public companies should make prices higher than they otherwise would be, as there are fewer sellers or at least less depth in the market," said Jay Stevens, director of market analytics at Aegis Hedging, which helps producers and consumer companies with their strategies.

The trend may also mean less business for banks and brokers that execute the hedges for producers.

Hedging volumes across US producers have declined by about 1 million barrels a day since 2019, equating to roughly 365,000 contracts over a year. That's more than 20% of the current open interest on West Texas Intermediate futures, which is already down by about 1 million contracts from a record set in 2018.

To be sure, the volume of hedging is largely dropping from the public companies. Private companies are still actively hedging, market participants and consultants said.

"The small privates that borrow proportionately more and depend on private equity have less autonomy, so if they are forced to hedge by their sponsor, they will," said Steve Sinos, managing partner at Blue Lacy Advisors.

High prices left many drillers not needing their contracts last year, according to BNEF, which estimates that $47 billion has been spent on WTI, Brent and Henry Hub contracts in the last two years.

Even before the flurry of deal activity, shale producers had focused less on expanding production, reducing their need to lock in future prices as banks has often required them to do when lending for new projects. They've instead plowed cash into reducing debt and boosting payouts to shareholders - a discipline they've pledged to continue.

"As we continue to drive debt down, we'll drive that hedging level down from that sort of 50% and 40% down back toward a quarter to a third of production," Ovintiv Inc. Chief Executive Officer Brendan McCracken said on an earnings call earlier this year.

Contact Us:

info@iadd-intl.org

3322 Hideaway Lane

Spring, TX 77388