By Emalee Springfield

•

02 May, 2024

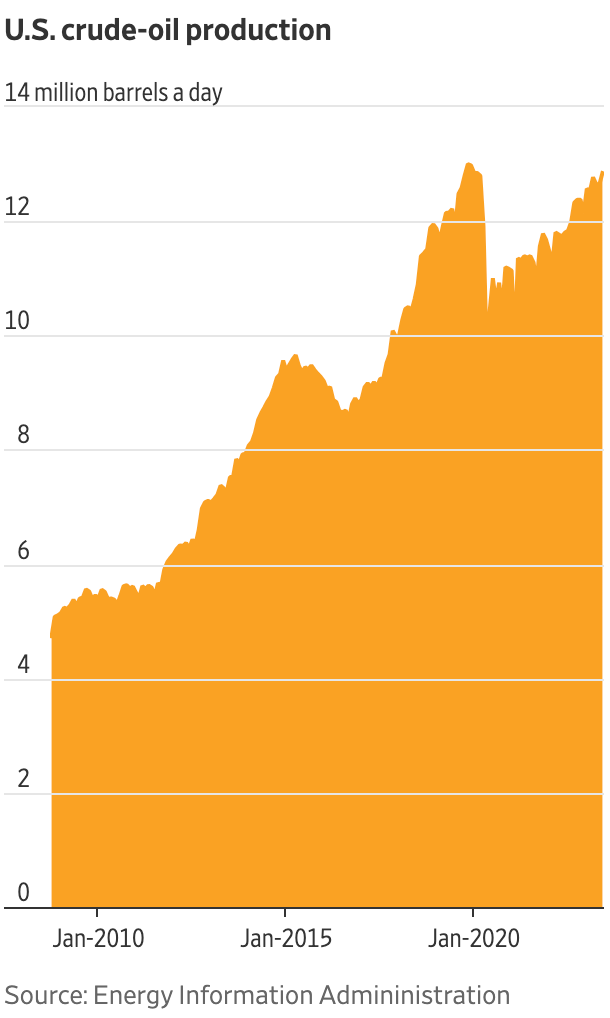

HOUSTON, April 30 (Reuters) - Oil prices fell 1% on Tuesday, extending losses from Monday, on the back of rising U.S. crude production, as well as hopes of an Israel-Hamas ceasefire. Brent crude futures for June, which expired on Tuesday, settled down 54 cents, or 0.6%, at $87.86 a barrel. The more active July contract fell 87 cents to $86.33. U.S. West Texas Intermediate crude futures were down 70 cents, or 0.9%, at $81.93. The front-month contract for both benchmarks lost more than 1% on Monday. U.S. crude production rose to 13.15 million barrels per day (bpd) in February from 12.58 million bpd in January in its biggest monthly increase since October 2021, the Energy Information Administration said. Meanwhile, exports climbed to 4.66 million bpd from 4.05 million bpd in the same period. U.S. crude oil inventories rose by 4.91 million barrels in the week ended April 26, according to market sources citing American Petroleum Institute figures on Tuesday. Stocks were expected to have fallen by about 1.1 million barrels last week, an extended Reuters poll showed on Tuesday. Official data from the EIA is due on Wednesday morning. Gasoline inventories fell by 1.483 million barrels, and distillates fell by 2.187 million barrels. Expectations that a ceasefire agreement between Israel and Hamas could be in sight have grown in recent days following a renewed push led by Egypt to revive stalled negotiations between the two. However, Israeli Prime Minister Benjamin Netanyahu vowed on Tuesday to go ahead with a long-promised assault on the southern Gaza city of Rafah. "Traders believe some of the geopolitical risk is being taken out of the market," said Dennis Kissler, senior vice president of trading at BOK Financial. "We're not seeing any global supply being taken off the market." Continued attacks by Yemen's Houthis on maritime traffic south of the Suez Canal - an important trading route - have provided a floor for oil prices and could prompt higher risk premiums if the market expects crude supply disruptions. Investors also eyed a two-day monetary policy meeting by the Federal Reserve Open Market Committee (FOMC), which gathers on Tuesday. According to the CME's FedWatch Tool, it is a virtual certainty that the FOMC will leave rates unchanged at the conclusion of the meeting on Wednesday. "The upcoming Fed meeting also drives some near-term reservations," said Yeap Jun Rong, market strategist at IG, adding that a longer period of elevated interest rates could trigger a further rise in the dollar while also threatening the oil demand outlook. Some investors are cautiously pricing in a higher probability that the Fed could raise interest rates by a quarter of a percentage point this year and next as inflation and the labor market remain resilient. U.S. product supplies of crude oil and petroleum products, EIA's measure of consumption, rose 1.9% to 19.95 million bpd in Feb. However, concerns over demand have crept up as diesel prices weakened . Balancing the market, output from the Organization of the Petroleum Exporting Countries has fallen in April, a Reuters survey found, reflecting lower exports from Iran, Iraq, and Nigeria against a backdrop of ongoing voluntary supply cuts by some members agreed with the wider OPEC+ alliance. A Reuters poll found that oil prices could hold above $80 a barrel this year, with analysts revising forecasts higher on expectations that supply will lag demand in the face of Middle East conflict and output cuts by the OPEC+ producer group. View on the Reuters Website